Decline in the inequality of Bank account ownerships in India

The percentage of adults having bank account ownership is an important indicator to understand the financial penetration in an economy. The access to the financial world will help the individuals of an economy to transact and manage money through savings, investments, making payments, and borrowing which would further enhance their financial well-being. Access to the bank account is the first step in this process but to ensure that the needs are met, it is vital to improve the financial literacy and at the same time reduce the inequality that persists and strategically expand the activities of financial inclusion.

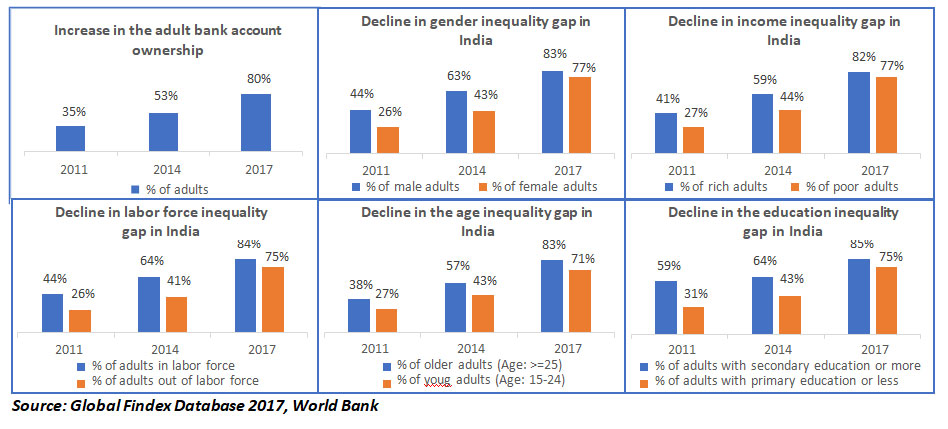

Globally, there is a rise in financial inclusion. As per the World Bank’s Global Findex database 2017, over 80% of the adult population in India have bank account ownership and the rest 20% are unbanked. Among the 80% of the banked population in India, the inequality gap persists. However, the data reveals that there is a drastic decline in the inequality gaps of the bank account ownerships in India.

- Adult men have a higher percentage of bank account ownership compared to adult women. The gender inequality gap has shrunk in India from 18% in the year 2011 to 6% as of

- Adults among the richest 60% of the population have higher percentage of bank account ownership compared to the adults among the poorest 40% of the population. The income inequality gap between rich and the poor in India has reduced from 14% in the year 2011 to 5% as of

- Adults in the labor force have a higher percentage of bank account ownership compared to the adults out of the labor force. The labor force inequality gap has reduced from 18% in the year 2011 to 9% in the year

- Older adults (Age >=25) have a higher percentage of financial account ownership than the Young adults (Age between 15-24). The age inequality gap has increased from 11% in the year 2011 to 14% in the year 2014 and then declined to 12% as of

- Adults with secondary education or more have a higher percentage of bank account ownership than adults with primary education or less. The education inequality gap has reduced from 28% in the year 2011 to 10% in the year

Cheers to the Government of India, an increase in the bank account ownership and decline in the inequality gaps has become possible because of the focused financial education and financial inclusion initiatives. The likelihood of banking the unbanked and further decline in the inequality gaps in India is higher in the future report of Global Findex database due to the recent financial inclusion initiatives such as National Strategy for Financial Education (NSFE) 2020-2025 , Pradhan Mantri Jan-Dhan Yojana (PMJDY), social security schemes viz. Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), Atal Pension Yojana (APY), Pradhan Mantri Kisan Maan Dhan Yojana (PM-KMY), Pradhan Mantri Shram Yogi Maan Dhan Yojana (PM-SYM) and Pradhan Mantri Mudra Yojana (PMMY) that are trying to bring the excluded sections into the financial mainstream.

In the face of the challenges due to COVID-19 pandemic, ensuring effective implementation of the financial inclusion initiatives, monitoring and expanding the reach of the financial education initiatives, and deeper penetration of mobile and internet access should be the key areas of focus for the regulators and the Government of India.

Dr. Muneer Shaik is an Assistant Professor at Mahindra University, School of Management, Hyderabad.

Read Your Next Blog

How Artificial Intelligence is Shaping the Next Generation of Engineers for Industry 4.0

How BBA LL.B. Degree can Help You Shape Law, Understand Business and Lead the Future

")

Shape Narratives, Build Brands & Lead Media with a BA in Journalism and Mass Communication

B.A. LL.B. Course Details: Duration, Fees, Subjects, Syllabus, and Admission 2025

Course Where Art Meets Technology")

Unveiling the World of Hospitality Management: Crafting Memorable Experiences

What is Journalism and Mass Communication: Crafting Stories That Shape the World

How to Become a Lawyer: A Step-by-Step Guide to a Rewarding Legal Career

Be a Master of the Smallest Particle Alive and Know What is Nanotechnology

Engineering Aspirations: Your Guide to B.Tech Courses and Admissions 2025

Mastering the Law: Your Ultimate Guide to the 3-Year LLB Course Syllabus

Take a Flight to Success by Knowing the Answer of What is Aerospace Engineering

LL.B. Course Details: Everything You Need to Know to Kickstart Your Legal Career

From Classrooms to Coding: Courses After 12th Computer Science for Aspiring Tech Wizard

What is Mechanical Engineering: The Science Behind Machines and Mechanics

From Courtrooms to Corporate Offices: Government Jobs You Can Land with a BBA LL.B.

Essential BBA Course Details: All You Need to Know About Business Studies

Design the Future with a B.Des – Where Creativity and Strategy Collide

Explore the Future: Top B.Tech. Courses to Kickstart Your Engineering Career

From Guest Services to Executive Suites: Navigating Your Journey with B.Sc. in Hospitality Management Course

From Resorts to Restaurants: Exploring Jobs After Hospitality Management

From Data to Discovery: How Biomedical Data Science is Accelerating Breakthroughs in Medicine

Step into the World of Finance: Your Guide to BBA Finance Admissions and Opportunities

Climbing the Academic Ladder: Your Ultimate Guide to Doing a Ph.D. in India

Power Up Your Potential: Best Engineering Courses After 12th For Tech Enthusiasts

System Engineering: Building a Resilient Career in a Rapidly Changing World

Making the Right Choice: Exploring the Best Career Options After 12th Grade

")

More Than Just Litigator: 10 Rewarding Career Options After B.A LL.B. (Hons.)

Develop Media Literacy and Form a Career in Journalism and Mass Communication

Is Mechanical Engineering a Good Career? Exploring Career Paths & Benefits

Innovate Infrastructure Development – Different Types of Civil Engineering

Give a Boost to Your Technologically-advanced Career with M.Tech. Courses

Different Types of MBA Courses – Gain Valuable Skills for the Business World

Elevate Your Leadership Expertise with a Doctorate in Business Administration

Lay a Solid Foundation for Your Career with the Exploration of Types of Mechanical Engineering

Embrace the Science of Healing and Innovation with Biotechnology Engineering Scope

Discern Your Dream Career in Media with the Scope of Journalism and Mass Communication

Exploring Law Courses After 12th: Your Gateway to a Diverse Legal Landscape

The Power of Connectivity: Unveiling the Scope of Electronics and Communication Engineering

Exploring the Expansive Horizons: The Scope of Journalism and Mass Communication

Achieving Educational Excellence: A Deep Dive into Master’s Degree in Education

Beyond the Degree: Unveiling the Multifaceted Benefits of Doing an MBA

Bridging Gaps, Building Futures: Exploring the Endless Scopes of Civil Engineering

Choosing Your Legal Path: BA LLB vs BBA LLB – Which Course is Better?

Kickstart Your Journey With Mass Communication Courses After 12th Grade

Decoding the Difference Between Electrical and Electronics Engineering

Next Steps: Exploring Top Computer Science Engineering Courses After 12th

Journalism Courses After 12th – Understanding the Significance of a BA in Journalism and Mass Communication

Forge Your Path to Excellence with Ph.D. Admission – Dive Into Details

Why MBA After Engineering: Transcending from Technical Wizardry to Leadership Mastery

Know the Scope of PhD in Economics and uncover hidden patterns of economic brilliance.

A Closer Look Into the BBA Computational Business Analytics Admission Process

From Circuits to Codes – Discover a Wide Range of Career Options After B.Tech. ECE

The Nanotech Revolution: The Astonishing Future Impact of B.Tech. Nanotechnology

From Roads to Skies: The Limitless Horizon of the Scope of M.Tech. in Transportation Engineering

Discover a New Era of Business Education with the Immense Scope of BBA in Computational Business Analytics

From Application to Acceptance – Navigate the Ph.D. Information Science and Technology Admission Process

Pave Your Path to Financial Brilliance with an Enormous Scope of BA Economics and Finance

Join the Digital Revolution with Diverse Career Options After B.Tech. ECE

Discover Your Eligibility for B.Tech. Biotechnology and Kickstart Your Career

Transform Your Career Trajectory with the Lucrative Scope of an Executive MBA

")

M.Tech. in Power Electronics and Renewable Energy Systems – Pursue New-age Careers

Ph.D. in Economics – Discover Innovative Solutions to Economic Challenges

M. Tech. in Autonomous Electric Vehicles – Dive Into the Future of Autonomous Vehicles (AV)

Construct a Better World with B.Tech. in Civil Engineering from Mahindra University

Acquire the Futuristic Mathematical & Computing Technologies with a Computational Mathematics Course

PhD in Business Administration – Dig Deeper into the Science of Management

B.Tech in Mechanical Engineering – Become a Master of Mechanics at Mahindra University

Shape Your Engineering Career with Mahindra University – One of the Best Engineering Colleges in Hyderabad

Transform Lives & Shape the World with Mahindra University – One of the Top Civil Engineering Colleges in Hyderabad

B Tech in Artificial Intelligence – The Next Big Thing in Technological Revolution

Lead the Tech Revolution with BTech CSE at Mahindra University – One of the Best Computer Science Engineering Colleges in Hyderabad

Kickstart Your Legal Career with Mahindra University – One of the Best Colleges for BBA LLB

Top BA LLB Colleges in Hyderabad – Training Exceptional Lawyers and Leaders

BTech Electronics and Computer Engineering Course – Engage in Independent and Life-long Learning

Best Colleges for Humanities and Social Sciences – Get World-class Training and Hands-on Learning Experience

![Arm_Yourself_with_Deep_Business_Knowledge_&_Insights_with_PhD_Program_in_Business_Administration_at_Mahindra_University[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/Arm_Yourself_with_Deep_Business_Knowledge__Insights_with_PhD_Program_in_Business_Administration_at_Mahindra_University1.jpg "Arm_Yourself_with_Deep_Business_Knowledge_&_Insights_with_PhD_Program_in_Business_Administration_at_Mahindra_University[1]")

Arm Yourself with Deep Business Knowledge & Insights with PhD Program in Business Administration at Mahindra University

![Emerge_as_a_Forward_thinking_Mechanical_Engineer_with_B_1140x460[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/Emerge_as_a_Forward_thinking_Mechanical_Engineer_with_B_1140x4601.jpg "Emerge_as_a_Forward_thinking_Mechanical_Engineer_with_B_1140x460[1]")

Emerge as a Forward-thinking Mechanical Engineer with B.Tech in Mechanical Engineering at Mahindra University

![B.Tech_in_Computer_Science_Engineering_(BTech_CSE)_Your_Gateway_to_Become_a_Computer_Genius_1140x460[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/B.Tech_in_Computer_Science_Engineering_BTech_CSE_Your_Gateway_to_Become_a_Computer_Genius_1140x4601.jpg "B.Tech_in_Computer_Science_Engineering_(BTech_CSE)_Your_Gateway_to_Become_a_Computer_Genius_1140x460[1]")

B.Tech in Computer Science Engineering (BTech CSE) – Your Gateway to Become a Computer Genius

![Digital_Marketing_is_Booming_Globally_1140x460[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/Digital_Marketing_is_Booming_Globally_1140x4601.jpg "Digital_Marketing_is_Booming_Globally_1140x460[1]")

The Scope of Digital Marketing is Booming Globally. Transform the Business Landscape with a BBA in Digital Marketing

![MU_Electrical20Computer20Engineering_1140x460[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/MU_Electrical20Computer20Engineering_1140x4601.jpg "MU_Electrical20Computer20Engineering_1140x460[1]")

India Calls for Multitalented Engineers. Be the One with the Electrical and Computer Science Engineering Course

![BA_LLB_Hons_Course_at_Mahindra_University[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/BA_LLB_Hons_Course_at_Mahindra_University1.webp "BA_LLB_Hons_Course_at_Mahindra_University[1]")

Do You Want to Pursue Law as a Career? Take BA LLB Hons Course at Mahindra University

![Management_&_Business_Administration_is_Tremendously_High[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/Management__Business_Administration_is_Tremendously_High1.jpg "Management_&_Business_Administration_is_Tremendously_High[1]")

The Scope of PhD in Management & Business Administration is Tremendously High. Understanding the Significance.

Civil Engineers Are New-age Superheroes. How is Mahindra University Moulding Futuristic Civil Engineers?

![whyistraining&placementcellimportant[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/why20is20training2020placement20cell20important1.png "whyistraining&placementcellimportant[1]")

![TheDifferencesbetweenRights&Duties[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/The20Differences20between20Rights2020Duties1.png "TheDifferencesbetweenRights&Duties[1]")

![sleep_deprivation[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/sleep_deprivation1.jpg "sleep_deprivation[1]")

![SelfLoveBlogImage2[1]](https://www.mahindrauniversity.edu.in/wp-content/uploads/2023/04/Self20Love20Blog20Image2021.png "SelfLoveBlogImage2[1]")

Be Legally Empowered by Pursuing Law | Top BA LLB (Hons) Colleges in Hyderabad

Pursue BA in Economics & Finance and contribute to India’s economic development

A Comprehensive Outlook On One Of The Highly Sought After Courses In Law: BBA LLB (Hons)

Why Revolutionary B.Tech Computer Science and Engineering Course Is The Choice Of Every Aspiring Student?

B.Tech in Computer Science & Engineering: A course for those who want to learn to lead forward

Manifesting excellent managerial skills and a fatter salary tag? It’s just a degree away.

Why BBA LLB is the right course for Law and Business enthusiasts in 2022

Here’s why B.Tech in Mechanical Engineering is one of the emerging courses for today’s talented youngsters

How Has Digital Marketing Turned Out To Be A Boon For Creative Individuals ?

Reasons Why You Should be active in Sports, Extracurriculars at The University

Skillsets That Give You an Edge Over Others in Securing Your Dream Job

Getting Back to Campus in The Post-COVID 19 World, 5 Hacks You Should Remember

How has Computer Science Engineering (CSE) evolved to create a demand among engineering aspirants

How B.Tech In Mechatronics Engineering Contributes In Making Human Life Easier?

Most Promising Engineering Disciplines with the Best Opportunities in 2025

")